What happened?

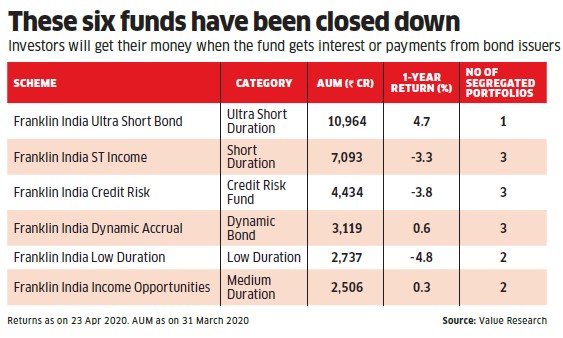

Franklin Templeton Mutual Fund has decided to wind up (read as permanently shut down) the following 6 schemes and return the money back to investors albeit with a delay.

- Franklin India Low Duration Fund (No. of Segregated Portfolios – 2)

- Franklin India Ultra Short Bond Fund (No. of Segregated Portfolios – 1)

- Franklin India Short Term Income Plan (No. of Segregated Portfolios – 3)

- Franklin India Credit Risk Fund (No. of Segregated Portfolios – 3)

- Franklin India Dynamic Accrual Fund (No. of Segregated Portfolios – 3)

- Franklin India Income Opportunities Fund (No. of Segregated Portfolios – 2)

Subscriptions and Redemptions have been stopped in the above schemes.

The key point to emphasize is that the realized money will be returned back to investors – extent depends on the valuations at which they are able to sell their underlying holdings. However there will be a time delay and this will happen in a staggered manner.

Why did this happen?

All these funds were running credit strategies – i.e a substantial portion of the funds were lent to lower credit rated corporates as they pay higher interest rates to borrow given their lower credit quality, which in turn means higher returns for investors.

This was an explicitly stated strategy of the above funds and in technical terms is called as “Managed Credit” or “Credit Risk” strategies.

However these lower rated credit quality papers are usually not very liquid (read as they cannot be sold immediately in the market and will mostly have to be held till maturity). So as long as investors stay with the fund and the underlying papers don’t default on their interest and principal payments, these funds were doing fine.

In recent times, given the weak credit environment, such credit funds were facing significant redemption pressure from investors as most of them were moving to safer higher quality debt funds.

This led to a situation where the above mentioned Franklin Templeton funds were not able to sell their underlying papers (due to the illiquid market conditions for lower credit papers) to meet redemptions.

If the fund did not close, then it would have been forced to sell its underlying illiquid papers at distress valuations to pay for the redemptions. This would have in turn led to significant NAV impact for existing investors in the fund.

Hence the fund house, in order to avoid distress selling and value erosion to existing investors has closed all the above funds and decided to return the money back to investors.

So the key reason is :

) Lower Credit Quality Exposure which is extremely illiquid

2) Continuous and Significant redemptions in recent times as investors were shifting to higher credit quality funds

What will happen to the money invested in these funds?

The fund house will now sell the underlying securities of all these funds over time and return the realized amount to their investors in a staggered manner.

How long will it take for the money to be returned back to investors?

The fund house has indicated that they would liquidate the portfolio holdings at the earliest opportunity taking into context the portfolio maturity (the average period of borrowing for the underlying securities) and the current risk averse and illiquid market scenario.

Once the market recovers, early exits via sale/prepayment will be actively explored by the fund house with a view to facilitate repayment prior to the maturity of the portfolio investments.

Will investors get the entire money back? Is there a possibility of value erosion?

This will depend on the valuations at which Franklin Templeton is able to sell its underlying holdings.

What happens to SIP and STPs in the above funds?

Since Franklin Templeton has stopped subscriptions and redemptions in the above 6 funds, the systematic investment plans (SIP) will stop automatically.

For investors doing systematic transfer plans (STP) via any of the above funds to transfer gradually into equity funds, the transfers to equity funds will stop. The money stuck in these debt funds will be returned back (to the extent realized by selling underlying securities) over time in a staggered manner as explained earlier.

What should investors in the above funds do?

There is no further action required with regards to these funds. The fund house will sell the underlying securities and return the realized money over a period of time in a staggered manner.

Can something similar happen to my existing funds? Should I be worried?

If your debt funds are invested in high credit quality securities (read as Sovereign, PSUs, AAA rated corporates, Reputed groups etc), these continue to remain safe and have adequate liquidity.

The market for higher quality papers has enough liquidity (further supported by RBI measures) unlike the market for lower credits. So the ability of these funds to handle redemptions if any, is significantly higher compared to credit risk oriented funds.

Our positive outlook on shorter duration high credit quality funds is derived from

- Banking Liquidity of around 7 lakh crores – This means banks are keeping a whopping Rs 7 lakh crs with RBI at a paltry 3.75% interest rate (under repo rate). This we believe at some point in time will be lent back to the corporates (given the attractive interest rate differential which the banks can earn) and can lower the yields (providing return kicker based on the extent of modified duration of the fund).

- Targeted Long Term Repo Operations conducted by RBI – where banks can borrow 1-3 year money at the existing repo rate (4.4%) and lend to specified category of corporates. This creates huge upcoming demand for corporate bonds is expected to help in the lowering of yields.

- Expectation of further rate cuts, given the low inflation expectation and growth slowdown.

- We also expect more actions from RBI which will support the liquidity scenario and can help in lowering of debt fund yields.

So, as long as you are invested in our recommended funds which have the highest credit quality portfolios and stable investor flows with no significant redemption pressure, you are well positioned to take advantage of the positive return environment in debt funds.

When should you worry?

However, you should be worried if your debt portfolio has exposure to credit oriented funds which have

- High exposure to lower rated credit papers

- Facing significant redemptions from investors in the recent months

If yes, you should immediately talk to your advisor, understand the context and take a decision on these funds.

How did help our investors in staying out of these funds?

Our advisory team has been sending out alerts regarding this exit for the past six months.

As a result of this, majority of our investors have exited these funds ensuring no impact to their portfolios during the current event

#9829025569 #SNPARASHAR